NBFC Compliance

4.9

Overview of NBFC Compliance

Lately, rbi compliances for nbfc have become more complex for NBFCs. There used to be a time when Non-Banking Financial Companies enjoyed benefits over banks. There was a time when NBFCs compliances were far simpler and lenient but after Sahara case, RBI has drafted new compliances for NBFCs and keep them under their screening. A portion of the significant rules are Securitization of Standard Assets and Guidelines for Private Placement of NBFCs. RBI is continuing putting forth attempts for preventing theory in NBFCs .

Non-Banking Financial Companies are registered under the Companies Act 2013, and are involve in the business of receiving deposits, loans and advances, acquisition of stock/bonds/shares, debentures and securities issued by the government. NBFCs are actively involved in the financial activities and are registered by the Reserve Bank of India. No NBFC can run their business without receiving the license from Reserve Bank of India.

Term ‘Principal Business’ in NBFC

The term ‘Principal Business’ stands for those financial activities where a company’s

financial assets comprises of more than 50 percent of the total assets and income from financial

assets derive is more than 50 percent of the gross income. Any company who fulfils both these

criteria is eligible to be registered as NBFC. However, the term principal business is not defined

by the RBI but RBI has make it clear that companies which are involve in financial activity can be

registered and supervised by RBI.

Hence, those companies which perform activities

related to agriculture, sale and purchase of goods, construction of immovable property, sale of

immovable property, industrial activity cannot be regulated and supervised by RBI because they do

not fall under the criteria of NBFC.

What are the regulations for non-deposit accepting NBFCs with assets less than ₹ 500 crore?

In the event that the NBFCs have not obtain any access to public funds and don't have any client interface will not be exposed to any guideline either prudential or lead of business guidelines.

NBFCs having client interface will be exposed uniquely to lead of business guidelines including FYC, KYC, if they are not getting access to public funds. As though they are getting to the open assets, they will be exposed to restricted prudential guidelines.

NBFCs which are associated with both open assets and client interface exist are exposed to both limited prudential and business guidelines.

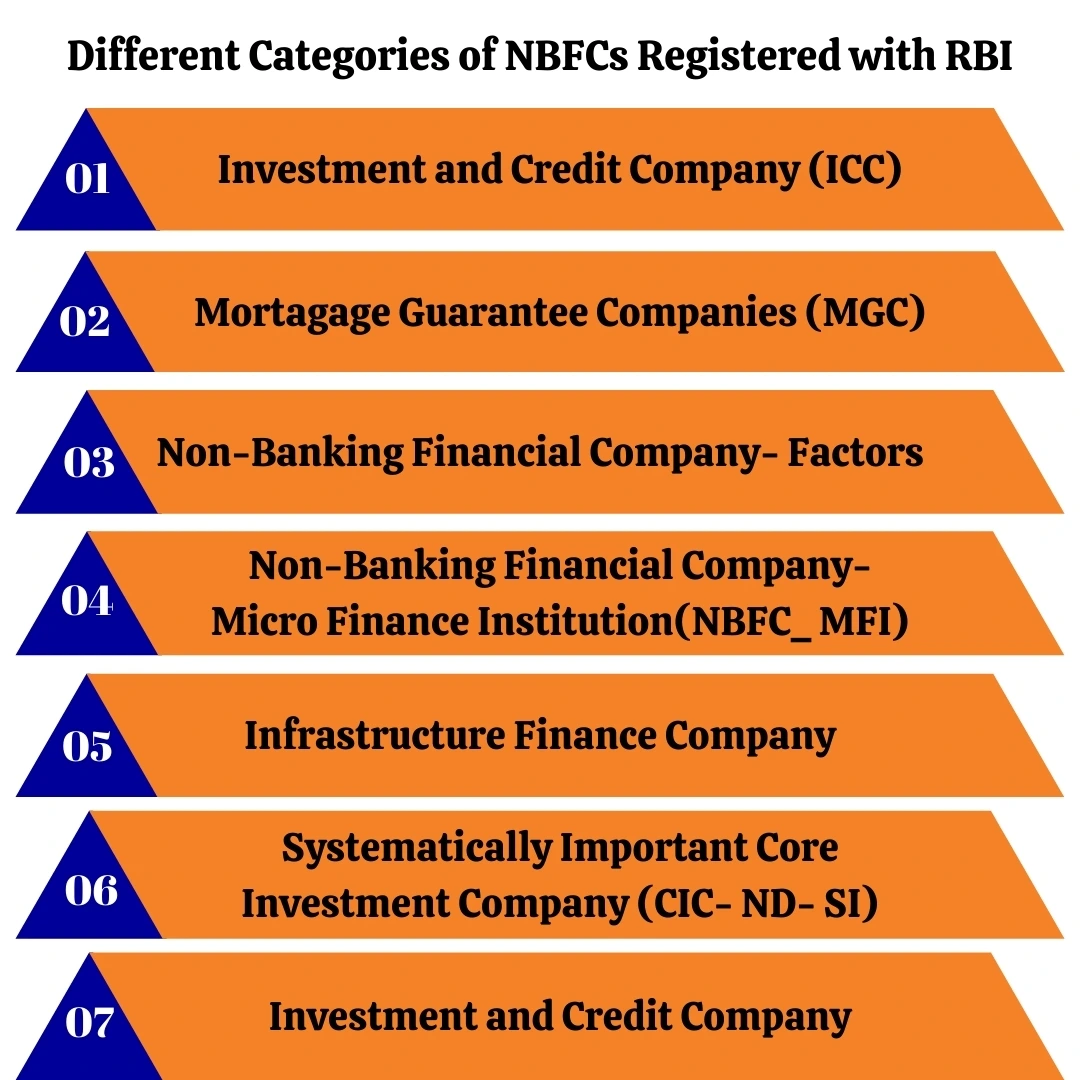

Different Categories of NBFCs Registered with RBI

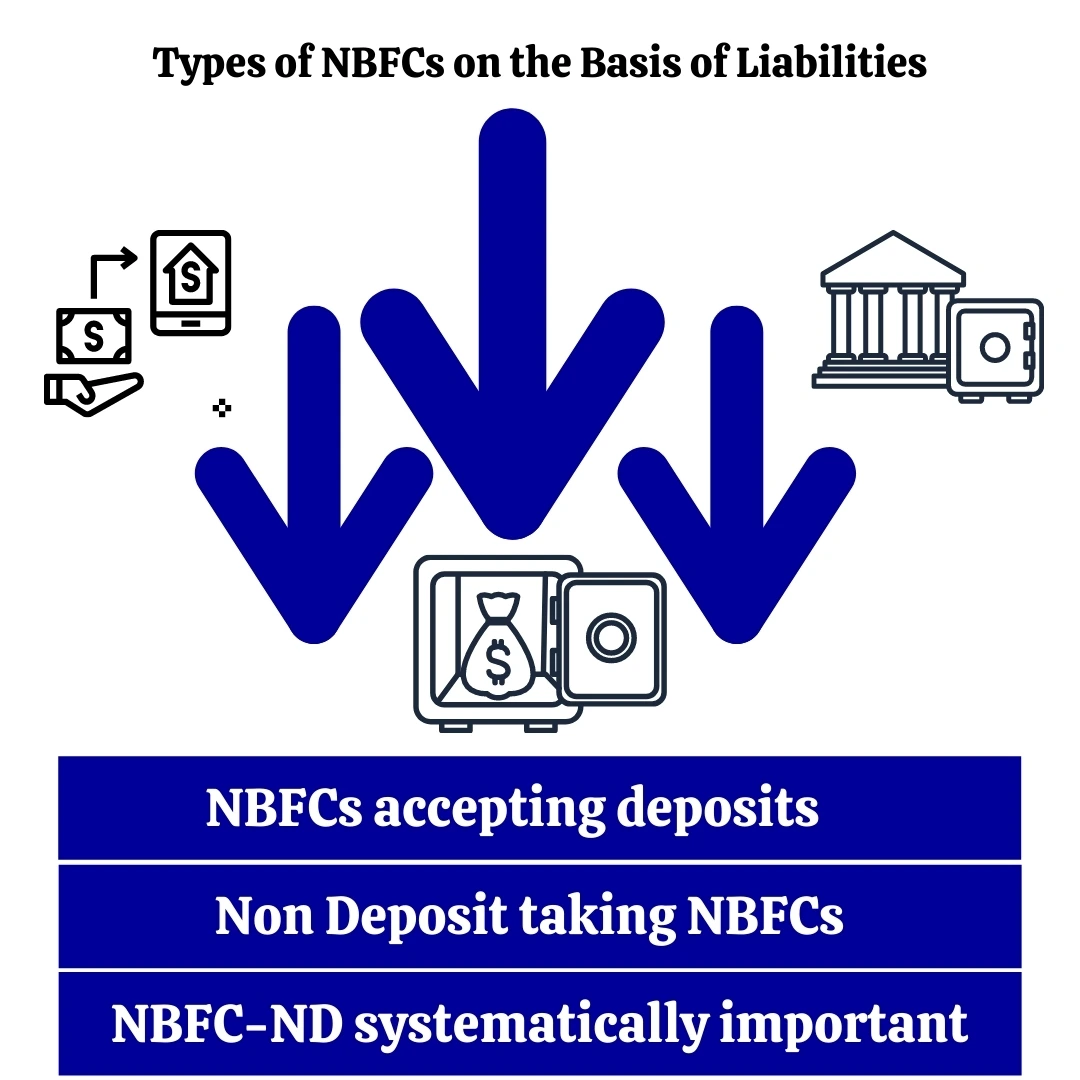

Types of NBFCs on the Basis of Liabilities

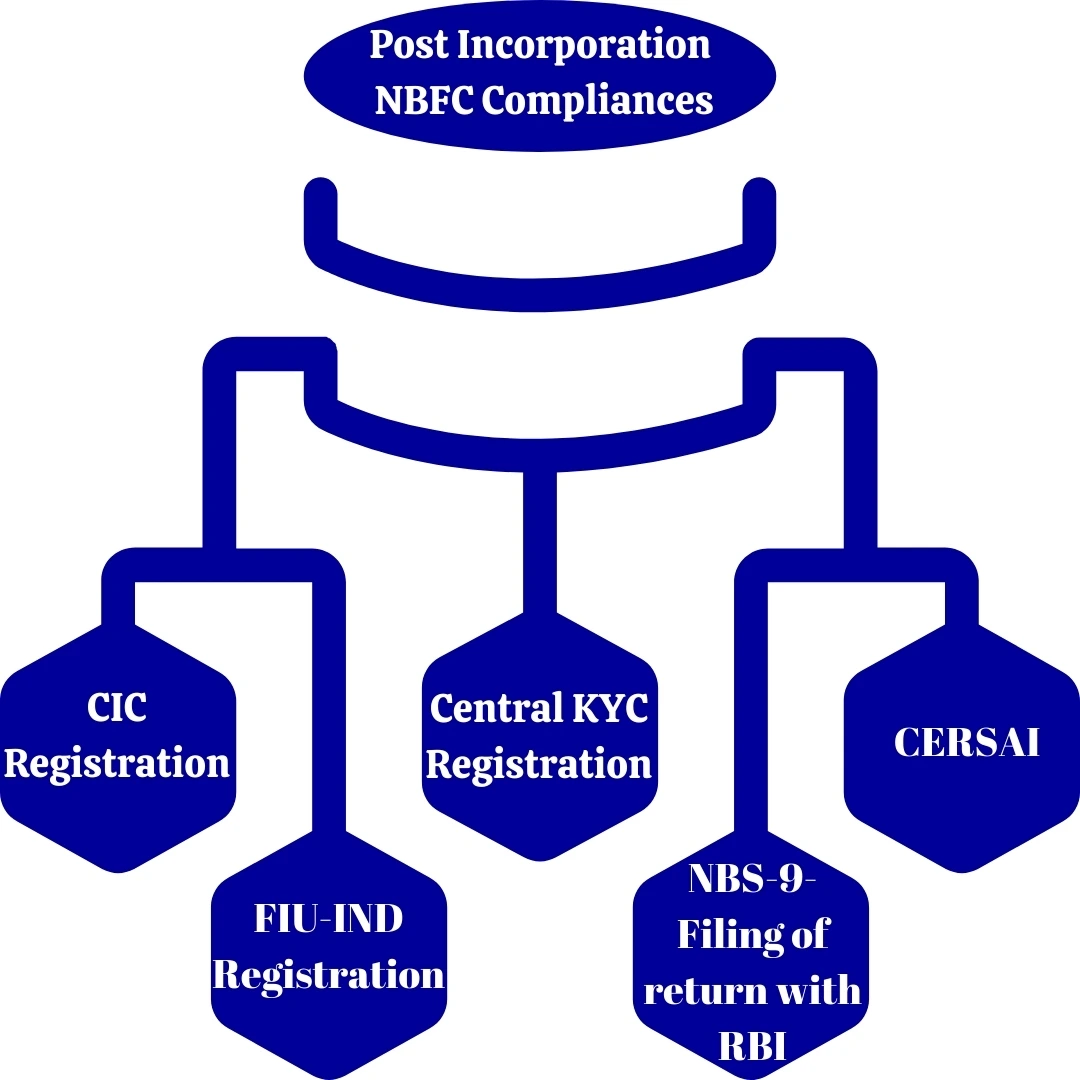

Post Incorporation NBFC Compliances

Once you have received a COR from the Reserve Bank of India, it time for NBFCs to become a member of all Credit Information Companies.

Adoption Of Fair Practice Code

The Reserve Bank India had disclosed its round dated September 28, 2006, gave rules on Fair Practices Code (FPC) for all NBFCs to be embraced by them while doing lending business. The rules secured general standards on sufficient exposures on the terms and conditions of a loan and furthermore embracing a non-coercive recuperation strategy.

CIC Registration

In India, below mentioned companies are treated as Credit Information Companies

CIBIL-Credit Information Bureau India Limited

CIBIL was introduced as India’s first Credit Bureau. To receive his/her credit score the person has to do a login onto the CIBIL website and provide the required details in an online form, the person will receive the credit score on the registered email id.

Equifax Credit Information Services Private Limited

Equifax has recorded its services in India in the year 2010 and has recorded a sublime development by assembling and absorbing the record of a person's monetary information and furthermore helps in dealing with the financial profiles of individual buyers.

Experian Credit Information Company Of India Private Limited

Experian does a credit check on its consumers and shows the probability of a consumer paying back capacity of his loan and credit.

CRIF High Mark Credit Information Services Private Limited

The purpose of CRIF High Mark is to ensure that the customer is trustworthy and there will be no flaws in the future operations. Mainly banks and lenders prefer credit rating companies.

FIU-IND Registration

Every NBFC, post incorporation requires Financial Intelligence Registration. It needs to provide their client details as given in the Prevention of Money Laundering Act. The reason behind doing FIU-IND registration is to give quality financial intelligence for the purpose of protecting the financial system from terror activities related to finance and other offenses which may include money laundering.

Central KYC Registration

Many NBFC s are quickly adopting the Central KYC registration, it is one of the most important NBFC compliance. The purpose of CKYC is to gather records for the customers in financial services. CERSAI which stands for Central Registry of Securitization and Asset Reconstruction and Security Interest, CERSAI is the registry authority for the Central KYC.

Obtaining Central KYC registration is essential for all the NBFCs in order to reduce the burden of the entity.

CERSAI

CERSAI additionally was known as Central Registry of Securitisation Asset Reconstruction and Security Interest of India. CERSAI has been built up as an organization under Section 8 of the Companies Act, 2013 by the Government of India.

CERSAI was framed to recognize and check any fraud activities during the lending transaction process against equitable mortgages. At the end of the day, the CRESAI was set up to demoralize and prevent the act of taking out different loans from a few banks utilizing a similar resource or property.

Submission Of Financial Information To Information Utilities

Section 215 of the IBC, 2016 gives methods to accommodation of financial information by lenders.

- It is obligatory for creditors to submit financial data and data identifying with resources corresponding to which any security intrigue has been made.

- It is discretionary for operational creditor to present the money related data to the information utility in such form as might be indicated.

Hence, any individual who expects to:

- present the financial data to the data utility; or

- get access to information from the data utility

will pay fee and submit data in such form and way as might be indicated by guideline.

Annual Compliance

NBS-9-Filling Of Return With RBI

NBFCs-ND file for NBS-9 and that’s too in case where there asset size is less than Rs 100 crore.

Convene Statutory Meeting

Statutory Meeting is convened so as to accord the investors an open door for seeing what level of progress has accomplished the floatation of the organization and all together that any uncommon issues requiring their endorsement might be laid before them.

The statutory gathering is held to advise the investors on the matters identifying with incorporation, allocation of offers, contracts went into by the organization, use of assets and so on.

Maintenance Of Accounts

Books of accounts including vouchers and receipts are required to be kept up under various legal laws - Income Tax Act, Companies Act 2013 and GST Act. Books to be kept up, maintenance period and compulsion necessities are distinctive under all the 3 laws.

GST Return Filing

A return is a record containing subtleties of pay which a citizen is required to file with the tax administrative authorities. This is utilized by tax authorities to ascertain tax obligation.

Under GST, an enlisted vendor needs to record GST returns that include:

- Purchase

- Sales

- GST (On sales)

- Input tax credit (GST paid on purchase)

- GST file return cannot be filed without sales and purchase invoices.

Income Tax Return Filing

An Income tax return (ITR) is a structure used to record data about your pay and expense to the Income Tax Department. The expense risk of a citizen is determined dependent on their salary. In the event that the return shows that an excess amount of tax has been paid during a year, at that point the individual will be qualified to get an income tax refund from the Income Tax Department.

According to the income tax laws, it is essential to file return each year by an individual or business that gains any income during a monetary year. The pay could be as compensation, business benefits, pay from house property or earned through profits, capital additions, premiums or different sources.

It is necessary for all the NBFCs incorporated under the Companies Act, 1956 to file their annual financial statement with MCA.

Annual Return Filing

Form AOC-4 NBFC (IND AS) & MGT-7 is used to file annual return with Registrar of Companies (ROC) within 30 days & within 60 days from conclusion of annual general meeting respectively.

Event Based Compliances

Change In Directors/ Registered Office/ Capital Structure

The process of change in directors/ registered office or any alteration in the capital structure is similar to that of ROC. To make any amendments in the above mentioned profiles all you have to do is adhere to the rules and regulations.

FDI

NBFCs allow 100% Foreign Direct Investment under automatic route but in some cases FDI is restricted.

Essential NBFC compliance Checklist for Non-Deposit and Deposit-taking Company

In The Case Of Annual Compliance nbfc compliance checklist

- Unaudited March Monthly return/NBS-7 on or before 30th June

- Statutory Auditors certificate on Income and assets with the time limit on or before 30th June

- Information about companies having FDI/Foreign Funds with the time limit on or before 30th June

- Audited March monthly return/NBS-7 filed upon completion

- File audited annual balancesheet and P &L Account with the time limit of one month from the date of signoff

- Resolution of Non-Acceptance of Public Deposit with the time limit of before the commencement of the new Fiscal tear

- Declaration of Auditors to Act as Auditors of the Company on annual basis

Monthly Compliance

Monthly return by 7th of every month

Periodical Compliances

- Appointment of Director time limit is within 30 days of appointment

- Resignation of Director (DIR-12+ challan report) with the time limit of within 30 days of appointment

- Adoption of any notification in the ensuing Board Meeting and filing the certified copy with RBI

Types of Returns

Returns By Deposit Taking NBFC

NBS-1

These are the Quarterly returns on deposit in the first schedule. Such return is required to be furnished for the purpose of capturing financial details such as Profit and Loss Account, Components of assets and Liability.

NBS-2

The Quarterly Return on prudential norms. The requirement to file this return is to get the details related to several norms like asset Classification, Capital Adequacy, NOF, Provisioning, etc.

NBS-3

The Quarterly Return on liquid assets. The intent behind filing such norms is to capture information about statutory investment in Liquid states.

NBS-4

The annual return of critical parameters which are by rejected companies those are holding public deposits. The objective behind filing this return is to find the repayment status of the rejected NBFCs accepting public deposits.

NBS-6

Needs to be filed as Monthly return on exposure to capital market by deposit-taking NBFC with the total assets of Rs. 100 crore or more.

ALM Return

These returns are file as Half-yearly by NBFC holding Public Deposit which is more than the amount of Rs. 20 Crore or asset size of more than Rs. 100 Crore.

- Requires Audited Balance Sheet and Auditor’s Report by NBFC accepting public deposits, to be furnished;

- Return related to branch Information

Returns By Non-Deposit NBFC

NBS-7

It is a quarterly statement providing information related to, risk assets ratio, capital funds, risk-weighted asset.

NBS-2

Such return is the Monthly return on a critical financial parameter of NBFCs-ND-SI.

ALM Returns

- Monthly- statement of short-term dynamic liquidity in format NBS-ALM-1

- Half Yearly- Statement of structural liquidity in format NBS-ALM2

- Half Yearly- Statement of interest rate sensitivity in format NBS-ALM-3

Branch Info Return

Quarterly return on important financial parameters of non-deposit taking NBFC having assets of more than ₹ 50 crores and above but less than ₹ 100 crores. The requirement like name of the company, address, Net Owned Fund, profit/loss during the last three years needs to be furnished quarterly by non-deposit taking NBFCs with asset size between ₹ 50 crores and ₹ 100 crores.

FAQ’s On NBFC Compliance

How do NBFC raise money?

NBFCs normally raise money from banks or sell business papers to shared assets to fund-raise. They on-loan these cash to little and medium enterprises, retail clients, etc.

Is LIC a NBFC?

Banks are BFCs (Banking and Financial Companies) where as LICI ( LIC of India, in case you are confused) is an NBFC. Bank is mainly deals with matter relating to deposit and lending while LIC provides a life insurance cover to the beneficiary.

What is the difference between NBFC and MFI?

NBFC represents non banking financial institutions that perform capacities like banks without banks in rustic regions. MFI represents miniaturized scale account establishments and the work at a further littler level than NBFC. MFI give little credits to the oppressed segments of the general public.

Is Insurance Company a NBFC?

Insurance companies are not NBFCs for a fundamental reason. They take cash from financial investors as protection premium, put resources into explicit protections as characterized by their regulator according to the sort of protection item and pay returns or claims to their customers.

Can NBFC give loan?

NBFCs can offer services such as loans and credit facilities, currency exchange, retirement planning, money markets, underwriting, and merger activities.

Can NBFC provide home loans?

Home loans offered by NBFCs are generally linked under the prime lending rate framework. On the flipside, banks are not permitted to loan beneath their MCLR values, however Non-Banking Financial Services are very free to do as such. Now and again clients may profit by lower loan fees also.

What is Central KYC registration?

Many NBFC s are quickly adopting the Central KYC registration, it is one of the most important NBFC compliance. The purpose of CKYC is to gather records for the customers in financial services. CERSAI which stands for Central Registry of Securitization and Asset Reconstruction and Security Interest, CERSAI is the registry authority for the Central KYC.

Who regulates NBFC in India?

The working and operations of NBFCs are regulated by the Reserve Bank of India (RBI) within the framework of the Reserve Bank of India Act, 1934.

Speak Directly to our Expert Today

Reliable

Affordable

Assured

Industries Served by

Professional Utilities

Apparels

Footwear

Furniture

Gems and Jewellery

Tourism & Hospitality

Consumer Electronics

Chemicals

Telecom

Oils & Gas

Hotel

Railways

Liquor

Health & Medical

Food Processing

Dangerous/ Haz. Goods

Tea & Coffee

Capital Goods

Recycling

Rubber

NGOs

Silk

Handloom

IT & BPM

Steel

Automobile

Tobacco

Constructions

Testimonials

"Explore how Professional Utilities have helped businesses reach new heights as their trusted partner."

It was a great experience working withProfessional Utilities. They have provided the smoothly. It shows the amount of confidence they are having in their field of work.

Atish Singh

![]()

![]()

It was professional and friendly experience quick response and remarkable assistance. I loved PU service for section 8 company registration for our Vidyadhare Foundation.

Ravi Kumar

![]()

![]()

I needed a material safety data sheet for my product and they got it delivered in just 3 days. I am very happy with their professional and timely service. Trust me you can count on them.

Ananya Sharma

![]()

![]()

Great & helpful support by everyone. I got response & support whenever I called to your system. Heartly thanx for Great & Super Service. Have a Great & Bright future of team & your company.

Prashant Agawekar

![]()

![]()

Thank you so much Professional Utilities team for their wonderful help. I really appreciate your efforts in getting start business. Pvt Ltd company registration was smooth yet quick.

Abhishek Kumar

![]()

![]()

I applied for Drug licence and company registration and their follow-up for work and regular updates helped me a lot. They are happily available for any kind of business consultancy.

Vidushi Saini

![]()

![]()

Great experience went to get my ITR done, process was quite convenient and fast. Had a few queries, am happy about the fact those people explained me all things I wanted to know.

Taniya Garyali

![]()

![]()

Great services provided by Professional Utilities. They are best in this industry and the best part is their prices are so affordable. Kudos to you. Now you guys are my full-time consultant.

Aftab Alam

![]()

![]()

Trusted By

.svg)