File Your TDS Return

4.9

TDS Return Filing Online - Types, Forms, Due Dates & Penalties

TDS return is a vital compliance procedure under the Income Tax Act that reflects all the TDS transactions carried out in a quarter. It allows for the proper reporting of taxes that have been withheld from payments made to employees, landlords, lawyers, interest earned, and contractors. The tax can only be deducted when the amount is credited to the payee’s account or when the payment is made whichever is the earliest.

Filing TDS returns on time and with correct information is important to avoid penalties and facilitate the process of tax credits to deductees. Some of the details include challan numbers, PAN information, and deduction amounts. Any mistake or delay relating to the return can attract charges, interest, or rejection of the return. The proper implementation of TDS return filing regulations allows for the enablement of efficiency, transparency, and reduced complaints, for both the deductors and recipients.

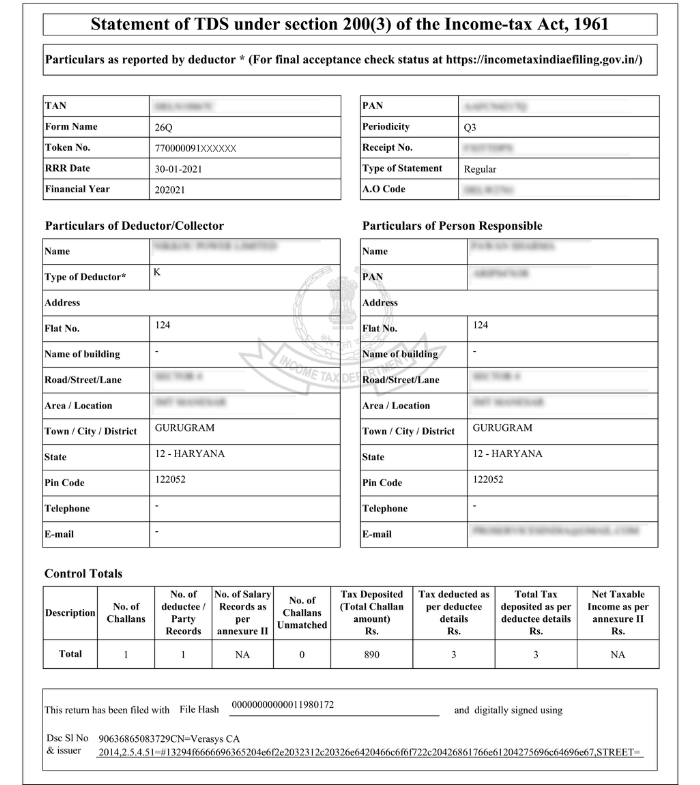

TDS Return Sample

Table of Content

- What is TDS Return?

- How to file TDS Return?

- Details Required to file TDS Returns

- What is a TDS Certificate?

- Types of TDS Return

- Due Dates For Filing TDS Return

- Penalty on Late or Non-Filing of TDS Return

- TDS Return Applicability/ Eligibility

- Benefits of TDS Payment

- TDS Return Correction Statement

- Conclusion

- Frequently Asked Questions

What is TDS Return?

TDS Return is a quarterly statement that needs to be submitted by the deductor to the Income Tax Department. The statement shows a summary of all the entries for TDS collected by the deductor and the TDS paid to the Income Tax Authority. The tax is required to be deducted at the time money is credited to the payee’s account or at the time of payment, whichever is earlier.

Usually, the person receiving income is liable to pay income tax. But the government with the help of Tax Deducted at Source provisions makes sure that income tax is deducted in advance from the payments being made. The recipient of income receives the net amount (after reducing TDS). The recipient will add the gross amount to his income and the amount of TDS is adjusted against his final tax liability. The recipient takes credit for the amount already deducted and paid on his behalf.

How to file TDS Return?

The step-by-step process to file TDS Returns online is as follows:

Step 1:Fill Form 27A

Form 27A contains multiple columns that must be filled properly. In case a hard copy of the form is filled, then it must be verified with the e-TDS return filed electronically.

Step 2: Matching Tax Deducted

Now, the tax deducted at source and the total amount that has been paid must be correctly filled and should be matched with their respective forms (24, 26, 27, 27A).

Step 3: Provide TAN

Next, the assessee that is filing the TDS return must mention the Tax Deduction Account Number (TAN) in Form 27A as dictated by sub-section (2) of section 203A of the Income Tax Act in India.

Note: It should be noted that the details like challan number, PAN of deductee, and the tax details must be mentioned on the TDS returns accurately because failing to do so would make the verification process more difficult.

Step 4: Filing e-TDS Form

The basic form that is used for filing e-TDS returns must be used because it brings consistency and better understanding in filling the forms and it is recommended by the department. It is necessary to mention the 7-digit Bank Branch Code to facilitate easy tallying.

Step 5: Submit TDS Return

Physical TDS returns must be submitted at the TIN-FC managed by NSDL. If returns are filed online, they can be submitted on the official website of the NSDL TIN. The deductor has to sign the TDS return through a digital signature.

Step 6: Receive Receipt or Rejection Memo

If all the information mentioned is correct, then a provisional receipt or token number would be issued. This is considered as an acknowledgment that confirms that the TDS return has been filed. In case the return is not accepted, then a non-acceptance memo along with the reasons for rejections is issued. In such cases, the TDS return must be filed again

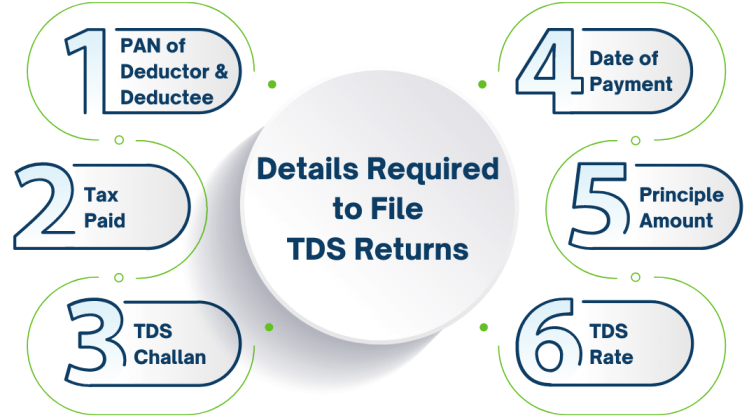

Details Required to file TDS Returns

To successfully file TDS (Tax Deducted at Source) Returns, you need the following key details:

-

PAN of the Deductor and Deductee

The Permanent Account Numbers of both the person deducting TDS and the person receiving income. -

Amount of Tax Paid

Exact details of the tax deposited with the government. -

TDS Challan Information

Challan reference number and related payment details. -

Date of Payment or Credit

The date on which the transaction was made or credited. -

Principal Amount on Which TDS is Deducted

The exact amount that forms the basis for TDS deduction. -

Rate of TDS Deduction

The applicable percentage of tax deducted at source.

What is a TDS Certificate?

TDS certificates have to be issued by the payer deducting TDS to the payee from whose income TDS was deducted while making payment. Form 16, Form 16A, Form 16B, and Form 16C are all TDS certificates.

| Form | Certificate of | Frequency | Due date |

| Form 16 | TDS on salary payment | Yearly | 31st May |

| Form 16 A | TDS on non-salary payments | Quarterly | 15 days from due date of filing return |

| Form 16 B | TDS on sale of property | Event based | 15 days from due date of filing return |

| Form 16 C | TDS on rent | Event based | 15 days from due date of filing return |

Types of TDS Return

There are four main types of TDS Return Forms under the Income Tax Act, 1961:

1. TDS Return on Salary Payments (Form 24Q)

- Form 24Q is filed quarterly by employers for TDS deducted on salaries under Section 192.

- It contains details of salary paid, TDS deducted, and challan information.

- Annexure-I (details of deductor, deductees, and challans) must be submitted for all four quarters.

- Annexure-II (salary details of employees for the financial year) is required only in the fourth quarter.

- Mandatory for all companies and firms in India to submit quarterly.

2. TDS Return on Payments Other Than Salary (Form 26Q)

- Form 26Q is filed for TDS on all payments excluding salaries. It is applicable under Sections 193, 194, and 200(3).

- Covers income such as interest on securities, dividends, professional fees, director’s remuneration, etc.

- Contains one annexure only (details of deductor, deductees, and challan).

- PAN is mandatory for non-government deductors. Government deductors should mention “PANNOTREQD.”

3. TDS Return on Payments to Non-Residents (Form 27Q)

- Form 27Q is filed quarterly for TDS deducted on payments to non-residents (NRIs/foreigners). It applies under Section 200(3).

- Covers payments such as interest, bonus, dividends, and any other income paid to NRIs.

- Non-government deductors must furnish PAN. Government deductors should use “PANNOTREQD.”

4. TDS Return on Collection of Tax at Source (Form 27EQ)

- Form 27EQ is filed for Tax Collected at Source (TCS) under Section 206C.

- Required quarterly with mandatory mention of TAN.

- Applies when sellers collect tax from buyers on specified goods/commodities.

- Tax can be collected on payments made via cash, cheque, credit, draft, or other modes.

- PAN is compulsory for non-government deductors. Government deductors should use “PANNOTREQD”

Due Dates For Filing TDS Return

The due dates for filing TDS return for FY 2025-26 are as follows:

| Quarter | Quarter Period | TDS Return Due Date |

| 1st Quarter | 1st April to 30th June 2025 | 31st July 2025 |

| 2nd Quarter | 1st July to 30th September 2025 | 31st October 2025 |

| 3rd Quarter | 1st October to 31st December 2025 | 31st January 2026 |

| 4th Quarter | 1st January to 31st March 2026 | 31st May 2026 |

Penalty on Late or Non-Filing of TDS Return

TDS return should be filed at the end of each quarter during the financial year. A person who fails to file the TDS/TCS return or does not file the return by the due dates prescribed under the Income Tax Act, then he is liable to pay late fees under section 234E. Apart from late filing fees, he would be liable to pay a penalty under section 271H too.

Late filing fees on TDS return (under section 234E)

As per section 234E, if a person fails to file the TDS/TCS return on or before the due date, then he shall be liable to pay a late filing fee of ₹200 for every day during which the failure continues. TDS return cannot be filed without payment of late filing fees which means the late filing fees shall be deposited before filing the TDS return.

The amount of late fees shall not exceed the amount of TDS. For instance, if the TDS amount is ₹5,000 and your late fee is ₹20,000, then you’ll have to pay a late filing fee of ₹5,000 only.

Note: ₹200 per day is not a penalty but a late filing fee.

As per section 271H, if a person fails to file the TDS/TCS return within 1 year from the due date of filing return, then the assessing officer may direct such person to pay a penalty under section 271H. The minimum penalty can be levied of ₹10,000 which can go up to ₹1,00,000.

Apart from the delay in filing TDS returns, section 271H also covers cases of filing an incorrect return. Penalty under section 271H can also be levied if a person has furnished incorrect information. The penalty levied in case of incorrect TDS return filing is a minimum of ₹10,000 and a maximum of ₹1,00,000.

Note: Penalty under section 271H will be in addition to late filing fees prescribed under section 234E.

TDS Return Applicability/ Eligibility

TDS returns can be filed by employers and organizations who have a valid Tax Deduction and Collection Account Number (TAN). Any person making specified payments mentioned under the Income Tax Act is required to deduct tax at source and deposit it to the Central Government within the stipulated time.

An assessee is liable to file a TDS return if TDS is deducted from his/her income. The assessees liable to file quarterly TDS return can be a company or people whose accounts are Audited u/s 44AB or he is holding an office under the Government.

Benefits of TDS Payment

TDS is payable on the earnings so it is important to note that the liability to pay TDS is applicable only in the event of earnings taking place. TDS is deducted before making payments. Deductions are to be made on payments that are made in cash, cheque, or credit. The amount deducted under TDS is further deposited with various government agencies.

Payment of TDS has various advantages which are as follows :

- Deducting TDS at source prevents tax evasion

- Tax collection is done duly and on time

- A large number of people come under the tax net

- The collection of TDS is a steady source of revenue for the government

TDS Return Correction Statement

If the original TDS return filed contains errors or incomplete information, the deductor must file a TDS Correction Statement.

Common mistakes that require correction include:

- Incorrect TAN (Tax Deduction and Collection Account Number)

- Wrong or mismatched PAN details of the deductee

- Errors in challan information

- Mistakes in the amount or nature of the transaction reported

To ensure compliance:

- A single correction statement must be submitted for each TAN per quarter.

- The correction must be filed with the Income Tax Department using the prescribed format.

- Timely filing helps avoid penalties, mismatches in Form 26AS, and notices from the department.

Conclusion

TDS returns is an essential compliance formality that every individual or business entity is required to fulfill in case of making specified payment under the Income Tax Act. Ensuring accurate filing within due dates helps avoid penalties and ensures smooth tax credit processing for deductees. Before filing TDS returns, businesses and deductors are also required to complete the TDS TAN Application online to obtain a valid TAN number for tax deduction and compliance purposes. Businesses seeking professional guidance can also Consult with Our CA to ensure accurate TDS compliance and hassle-free return filing. At Professional Utilities, we take care of all your TDS return filing needs and provide you with expert services to avoid any errors and ensure compliance and timely filing of the return. Our services are ideally suited for businesses, employers, or any other deductor who needs a convenient way of managing their TDS responsibility.

Frequently Asked Questions

How is TDS related to GST compliance in business transactions?

TDS (Tax Deducted at Source) and GST (Goods and Services Tax) are two important components of the Indian tax system that businesses must comply with. While GST applies to the supply of goods and services, TDS is deducted at the time of making specified payments. Understanding how both systems work together is important for accurate tax filing and compliance. To get a detailed explanation, you can refer to the TDS and GST guide for better clarity on their relationship and applicability.

What is 24Q and 26Q?

24Q is a quarterly statement of tax deducted at source from Salaries and 26Q is a quarterly statement of tax deducted at source from all payments other than salaries.

What is TDS Validation?

TDS Validation is the process of verifying TDS-related details such as PAN, certificate number, deduction rate, challan details, and lower/NIL deduction certificates before filing TDS returns.

What is a TDS Refund?

A TDS Refund is the amount refunded by the Income Tax Department when the Tax Deducted at Source (TDS) is higher than the actual tax liability of the taxpayer. The excess amount can be claimed by filing an Income Tax Return (ITR) for the relevant financial year.

Testimonials

"Explore how Professional Utilities have helped businesses reach new heights as their trusted partner."

It was a great experience working withProfessional Utilities. They have provided the smoothly. It shows the amount of confidence they are having in their field of work.

Atish Singh

![]()

![]()

It was professional and friendly experience quick response and remarkable assistance. I loved PU service for section 8 company registration for our Vidyadhare Foundation.

Ravi Kumar

![]()

![]()

I needed a material safety data sheet for my product and they got it delivered in just 3 days. I am very happy with their professional and timely service. Trust me you can count on them.

Ananya Sharma

![]()

![]()

Great & helpful support by everyone. I got response & support whenever I called to your system. Heartly thanx for Great & Super Service. Have a Great & Bright future of team & your company.

Prashant Agawekar

![]()

![]()

Thank you so much Professional Utilities team for their wonderful help. I really appreciate your efforts in getting start business. Pvt Ltd company registration was smooth yet quick.

Abhishek Kumar

![]()

![]()

I applied for Drug licence and company registration and their follow-up for work and regular updates helped me a lot. They are happily available for any kind of business consultancy.

Vidushi Saini

![]()

![]()

Great experience went to get my ITR done, process was quite convenient and fast. Had a few queries, am happy about the fact those people explained me all things I wanted to know.

Taniya Garyali

![]()

![]()

Great services provided by Professional Utilities. They are best in this industry and the best part is their prices are so affordable. Kudos to you. Now you guys are my full-time consultant.

Aftab Alam

![]()

![]()

Trusted By

.svg)