CBDT: No TDS on GST Component

This article deals with the CBDT clarification of no TDS on GST component in services invoices. It does NOT deal with the TDS payment under GST (TDS under GST will be deducted by government bodies).

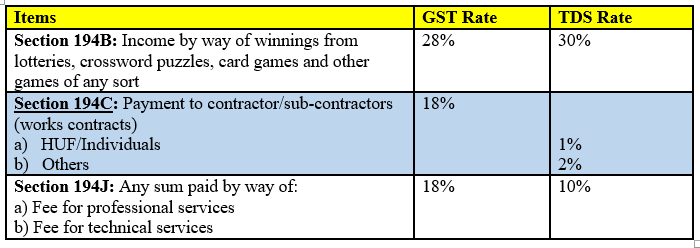

There are certain items on which GST apply along with provisions of TDS under income tax. Here’s a list of the items:

n other words, TDS would NOT be deducted on service tax component if the amount of service tax is shown separately in the invoice.As per circular No 1/2014 (issued by CBDT) TDS had to be deducted on the amount paid/payable without including service tax component.

After GST was implemented, CBDT received many queries on TDS on services and treatment of the GST component.

CBDT has clarified through Circular No. 23/2017 that if GST on services has been indicated separately in the invoice, then no tax would be deducted on GST component.

GST includes CGST, SGST, IGST, UTGST.

What does it mean?

There are certain payments as mentioned above, such as technical services which attract GST (18%) and which also attract TDS under Section 194J of the IT Act.

There was a lot of confusion whether TDS was going to be deducted on the full amount including GST or not. People feared that if GST was included before deducting TDS, it would lead to double taxation in the form of income tax on GST. This goes against the basic concept of double taxation avoidance under GST.

The CBDT has also clarified that this circular will also apply to existing contracts entered into before July 1.

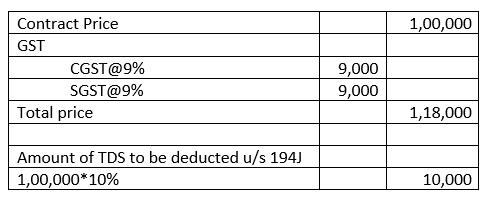

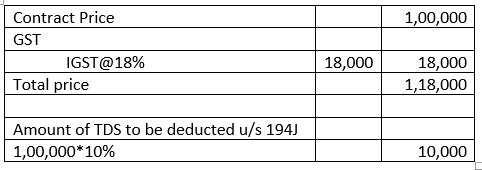

Example:

Ajay pays Rs. 1,00,000 construction fees to an engineer for construction of office building.

(Note: If the payment by an individual/HUF was for construction of residential building then TDS would not apply. Any other case, TDS applies)Example 1: Intra-state contract

Example 2: Inter-state contract

Example 3: GST is not shown separately

The reason for such a provision in the Income Tax Act, 1961 is to ensure that the GST paid by the service receiver does not form part of the income of the service provider.

Effect of this provision

The service provider only acts as a collecting agency for the government to collect GST.

Without this provision, the service receiver would charge TDS on GST and then the service provider would have to later claim refund of the same in the form of ITC.

The effect of such provision for the businesses (service providers) will mean less blockage of funds in TDS and thus reduce the working capital.

.svg)

Reliable

Businesses rely on us due to our Strong commitment to customer satisfaction.

Disclaimer:The information provided on this website is intended for general information purposes only. Although all reasonable efforts are made to ensure that the information provided is correct and reliable, it is not advised to be used as a substitute for professional advice. The information herein is not to be used in place of seeking professional services, counsel, or guidance. We highly advise that you consult a professional before you make any business or legal decisions regarding the information presented on this website. This website and its contents are given "as is", and we do not take any responsibility for any action that is taken based on information given on this website.

- Written by: Abhishek Yadav

- Fact-checked: Sahil Singh

- Updated on: March 31, 2026